Finance operations automation is the system that connects your accounting activity with the operational work that creates it. If your team still jumps between ERP screens, spreadsheets, inbox approvals, payroll files, supplier statements, and month-end reporting packs, finance operations automation is the missing link that turns all of that into one controlled flow.

What Finance Operations Automation Actually Means

Finance operations automation means using workflows, integrations, AI, and rules-based controls to move financial activity from transaction to approval to posting to reporting without constant manual intervention. The point is not just to digitise paper or speed up a single task. The point is to connect finance and operations so your numbers reflect what is actually happening in the business, in real time.

Think of it as the control layer between activity and accounting. A purchase request is raised, approved under the right authority, matched to an invoice, pushed into the accounting system, scheduled for payment, and reflected in a live dashboard. That is a connected process. Without that layer, finance stays reactive.

Why “operations” changes the conversation

Finance automation on its own usually means task automation inside the finance function. Invoice capture. Bank feeds. Scheduled reports. Useful, but narrow.

Finance operations automation is broader and more valuable. It covers the handoffs between departments, systems, and decisions. It connects procurement to payables, sales to receivables, payroll to project costing, and approvals to audit trails. That is where control either exists or falls apart.

This difference matters because most finance problems do not start inside the ledger. They start before the transaction hits the accounts. A poor approval path, missing purchase order, delayed timesheet, or disconnected sales update creates downstream mess. If you only automate the accounting step, you automate part of the problem.

The problem it solves for finance teams in Cyprus and Greece

This is a familiar picture across Cyprus and Greece: one accounting system, one payroll tool, several spreadsheets, too many email approvals, and reporting that arrives after the decision was needed. Add VAT pressure, multi-entity structures, local compliance demands, and growing operational complexity, and the finance team spends more time chasing information than controlling performance.

The result is predictable. Payables are unclear until late. Receivables visibility is patchy. Payroll checks become manual. VAT reviews turn into deadline pressure. Controllers cannot trust live numbers because live numbers do not exist.

That is why firms such as Prodyssey Solutions focus on business, finance, and technology as one operating model. The real issue is not a lack of software. It is the lack of connection between systems, workflows, and accountability.

Why Finance Automation Still Falls Short Without Connected Operations

Plenty of businesses say finance is automated. In practice, only pieces are. Research shows 54.2% of finance teams are still only partially automated. That is the real problem today, not total absence of technology, but fragmented automation that leaves the gaps untouched.

The cost of fragmented workflows

Fragmented workflows create slow approvals, delayed invoicing, repeated data entry, messy reconciliations, and weak audit evidence. A supplier invoice sits in an inbox because nobody owns the approval. A sales team confirms delivery, but finance does not bill immediately because the information never reaches the right system. A payroll adjustment is approved verbally, then entered manually, then checked again at month-end.

Each gap creates cost. Cash collection slows down. Month-end closes drag. Exceptions pile up. KPIs become inconsistent because each department uses a different version of the truth.

If you want a sharper view of where those gaps usually start, it helps to look at how finance and day-to-day operations connect. That connection is where speed, control, and reporting quality are won.

Why partial automation blocks ROI

Point solutions automate single steps, but they do not remove the handoffs in between. An OCR tool can read an invoice, but it does not fix broken approval rules. A bot can post entries, but it does not solve missing supplier master data. A dashboard can display KPIs, but it cannot make the underlying process reliable.

That is why ROI stalls. You pay for tools, but cycle times stay long because exceptions still need manual intervention. Error rates stay too high because source data is inconsistent. Cost per transaction barely moves because staff still spend hours validating, rekeying, and chasing approvals.

The strongest returns come from redesigning the whole process, not automating isolated tasks. If you need a framework for proving the commercial case with hard numbers, the right metrics are processing time, exception rate, close speed, compliance outcomes, and cost per invoice, not the number of automations deployed.

Which Finance Processes Deliver the Fastest Value

Not every process deserves attention first. The fastest value usually comes from high-volume, high-friction workflows where delays and errors directly affect cash flow, compliance, or management control.

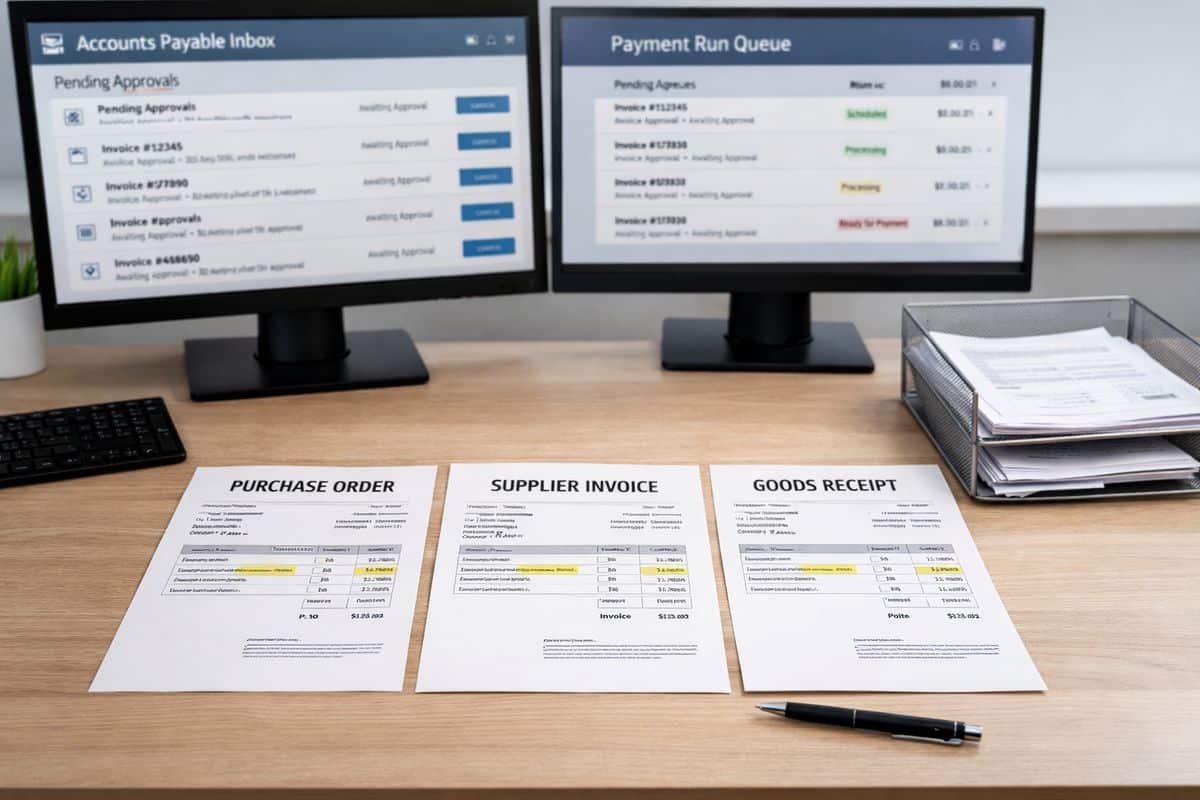

Purchase-to-pay and accounts payable

Accounts payable is usually the first win because the waste is easy to see. Supplier invoices arrive in different formats, approvals move through email, purchase orders are missing, and payment runs depend on manual checks.

Automation fixes this by capturing invoice data, routing approvals by rules, matching invoices against POs, flagging exceptions, and scheduling payments based on due dates and cash priorities. Benchmarks show manual AP can cost $12 to $18 per invoice, while automated processing drops that to $2 to $4 with much faster turnaround and better straight-through processing. That is not marginal improvement. That is operational control.

For SMEs handling growth, AP is often one of the best workflows to tackle early because the gains show up quickly in staff time, approval speed, supplier confidence, and spend visibility.

Order-to-cash and receivables visibility

Receivables automation matters for one reason above all: cash. If billing depends on manual triggers, customer records are inconsistent, or collections follow-up is ad hoc, your reported revenue and your actual cash position drift apart.

A connected order-to-cash flow links order confirmation, fulfilment, invoicing, payment tracking, and debtor reporting. You see who owes you, what is overdue, where disputes are stuck, and how collections affect forecast cash. Faster billing and cleaner follow-up improve working capital immediately.

This is where live dashboards stop being cosmetic. Real debtor visibility changes decisions about credit, purchasing, staffing, and investment.

Reconciliation, reporting, payroll, and tax workflows

Back-office friction hides in processes that feel unavoidable, but are not. Bank reconciliations, month-end close tasks, payroll checks, VAT preparation, and management reporting consume time because data arrives late and requires manual review.

Automation shortens the close by matching transactions faster, surfacing exceptions earlier, and feeding reporting directly from controlled workflows. Payroll becomes more reliable when time, leave, approvals, and cost centres connect properly. VAT and tax workflows become more defensible when source documents, coding logic, and approvals are traceable from start to finish.

In a region where tax discipline and reporting accuracy matter every month, this is not a nice upgrade. It is part of running a finance function properly.

The Technology Layer Behind Modern Finance Operations Automation

The technology matters, but only because it enables control. No CFO needs jargon. You need to know what the tools do and why the business gets better when they work together.

Workflow automation, OCR, RPA, and integrations

Workflow automation moves tasks through a defined route. OCR reads invoice and document data. RPA handles repetitive actions in older systems. Integrations connect your accounting platform with ERP, CRM, procurement, payroll, and operational tools.

Put together, these tools remove manual rekeying and reduce the chance of error. The wider automation market is expanding fast, with the digital process automation market projected to reach US$33.2 billion by 2030. That growth reflects a simple reality: businesses want workflows that move in real time, not through inboxes.

AI, machine learning, and exception management

Modern finance automation goes beyond task execution. AI and machine learning identify anomalies, predict outcomes, suggest coding, improve matching, and highlight exceptions that need attention. That shifts finance from reactive processing to active control.

But finance cannot run on black-box decisions. Explainability matters. Your team needs to know why an invoice was flagged, why a transaction was matched, and why an exception was escalated. Research shows 35.8% prioritise explainability because trust in finance systems depends on defensible logic and clean audit trails.

What Good Implementation Looks Like

Good implementation starts with process design, not software demos. Automation fails when you digitise confusion.

Start with process mapping and KPI baselines

Map the real workflow, not the ideal one. Where does work start, who approves it, where does it stall, what gets rekeyed, and which exceptions consume the most time? Then set baselines for processing time, error rate, exception rate, cost per transaction, and reporting lag.

Without that baseline, you cannot judge improvement. You also cannot prioritise properly.

Redesign the workflow before automating it

Bad processes do not become good because they are automated. If your approval matrix is vague, your supplier data is inconsistent, or your ownership lines are unclear, automation will simply make the confusion move faster.

That is why process redesign comes first. Standardise approvals. Define exception rules. Assign ownership. Tighten controls. Then automate. If your rollout also needs user buy-in, governance, and adoption discipline, making change stick in practice matters as much as the software itself.

Choose tools that scale across finance and operations

Choose platforms that support cloud access, role-based controls, live dashboards, ERP integration, auditability, and local compliance needs. Choose tools that can expand across entities, teams, and countries without rebuilding the logic every time.

This is one reason cloud deployment keeps gaining ground. Market data shows 58.3% cloud share in business process automation because scalable, connected platforms are easier to maintain, easier to access, and better suited to growing operations.

The Business Outcomes You Can Expect

When finance operations automation is done properly, the gains are visible at executive level.

Stronger cash flow, faster cycle times, better visibility

Approvals move faster. Invoices go out earlier. Collections become more disciplined. Spend is visible before payment day. Dashboards show payables, receivables, margins, and operational KPIs in one place.

That gives you faster decisions because the data is current, not reconstructed after the fact.

Higher accuracy, lower risk, cleaner compliance

Accuracy is the first priority for finance leaders, ahead of speed. That makes sense. Manual finance processes often carry error rates of 5 to 10 percent, and bad data spreads quickly across reports, tax submissions, and management decisions.

Connected automation reduces that risk through documented approvals, stronger controls, and traceable actions. You get cleaner VAT handling, better audit readiness, and more confidence in every number discussed at management level.

A finance team focused on insight, not admin

The value is not just lower admin effort. The value is what your team does with the time recovered. Instead of chasing approvals and checking duplicates, finance can focus on exceptions, forecasting, margin analysis, working capital, and decision support.

That is the shift that matters most. Admin-heavy finance reports the past. Connected finance operations help you steer the business now.

Common Risks, Misconceptions, and What to Watch

Automation is powerful, but poor design still kills projects.

Automation does not remove the need for finance judgement

Automation handles structured tasks and repeatable decisions. Your finance team still owns exceptions, policy interpretation, controls, commercial judgement, and escalation. That division is healthy. Machines process. Finance leads.

Bad data and weak governance will break automation

If master data is poor, approval rules are loose, and access controls are inconsistent, automation becomes unreliable very quickly. Data issues remain one of the most common barriers to success because the system can only enforce what your business has defined clearly.

The wrong metric is “how many tasks are automated”

That is a vanity metric. Success is lower processing cost, faster close, fewer exceptions, stronger compliance, better working capital, and more reliable management visibility. If those numbers do not improve, the project is not working.

How to Tell if Finance Operations Automation Is the Missing Link in Your Business

You do not need a theory exercise to know if the gap exists. The symptoms are obvious once you look at the flow instead of the functions.

Signs your current finance setup is holding back growth

Your team depends on spreadsheets to bridge systems. Month-end closes take too long. Approvals are unclear. VAT checks are manual. KPI reporting arrives late. Finance spends too much time asking operations for missing details. Cash visibility is weak until the last minute.

Those are not isolated frustrations. Those are signs that your finance model is disconnected from the business activity it is supposed to control.

What a connected finance operations model looks like

The target state is simple: one flow from transaction to approval to posting to reporting, with live dashboards, clear ownership, controlled exceptions, and audit-ready records. Finance and operations work from the same reality. Decisions are faster because the information is already connected.

That is the gap Prodyssey Solutions helps businesses close across Cyprus and Greece, by connecting systems, workflows, and financial control into one practical operating model. Once that link is in place, automation stops being a tech project and starts becoming how your business runs.

Leave a Reply